Bullion banks issue ZERO delivery notices on the April gold contract. Closing short positions may have lifted gold prices.

Bullion banks issue ZERO delivery notices on the April gold contract. Closing short positions may have lifted gold prices.

Starting with gold since the April gold contract is an active month and an inactive contract for silver …

++++++++++++++++++++++++ Gold

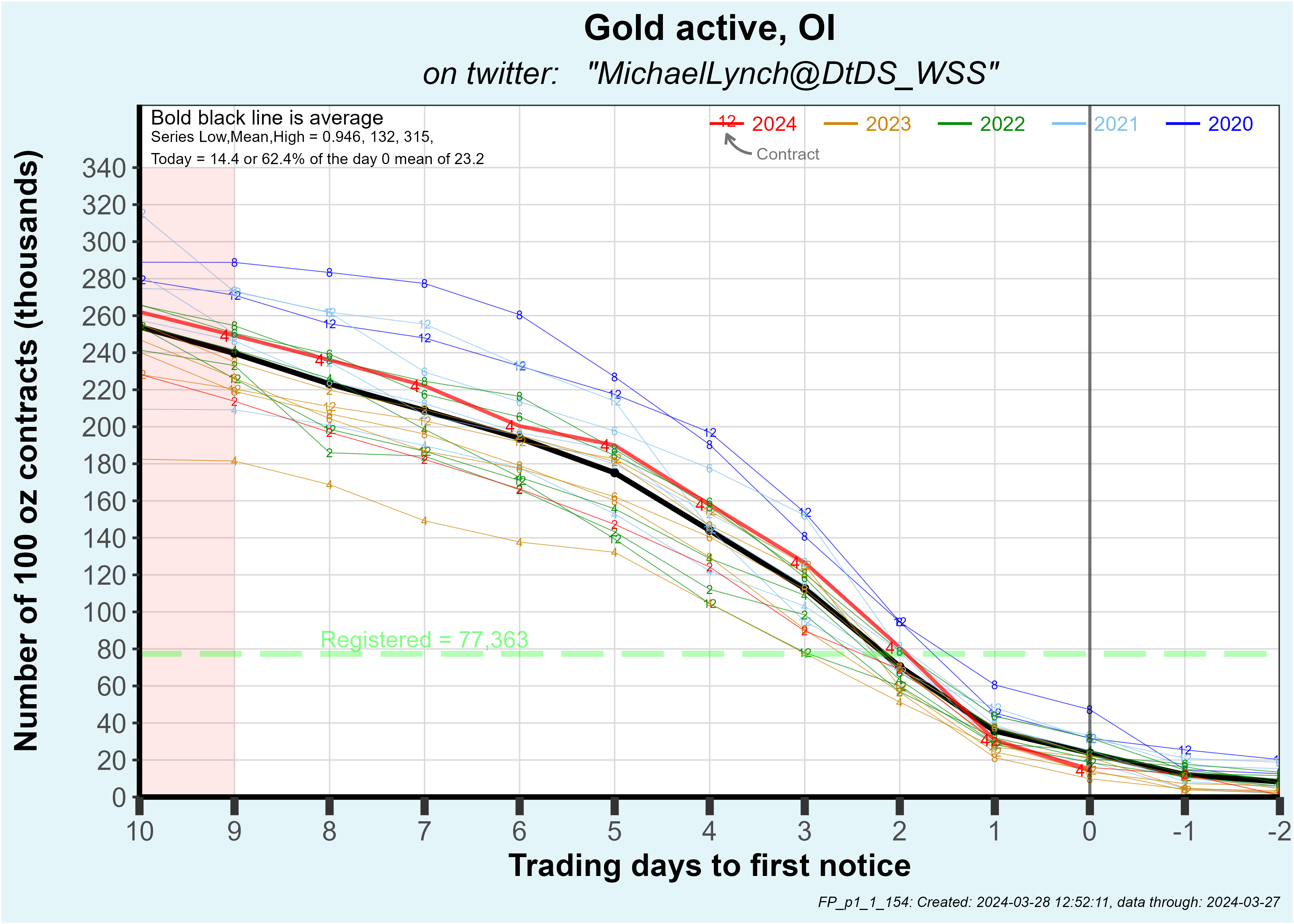

If you’ve been following my thread you know the April contract OI had been above trend until 2 days before first notice.

However, in the last 2 days before first notice, the OI reduction was much larger than average:

I have a hypothesis for this which explains both the OI reduction and gold price firmness.

To understand this consider segregating comex participants into 3 groups. First are paper traders who will roll their position no matter what. That group is NOT going to wait until the last days before first notice to roll. They start rolling at the start of the TAS surge about 17 days before first notice and likely finish soon thereafter as they’d not want to be forced to roll in the final days before first notice.

The second group would be physical commercial buyers or sellers like refiners. They would know in advance whether they were going to hold their short or long into first notice day or not, and, by definition, they will hold until first notice.

The third group are discretionary traders who have the option to hold until first notice day OR either close. I believe that this group is composed of mostly bankers. In support of that, I’d say that in the final days before first notice, the OI reduction on the roll contract is almost always much greater than the OI increase of the incumbent month. In other words … a lot of these late traders aren’t rolling at all, they are just closing a position. Who would have the discretion to to that? Bullion banks.

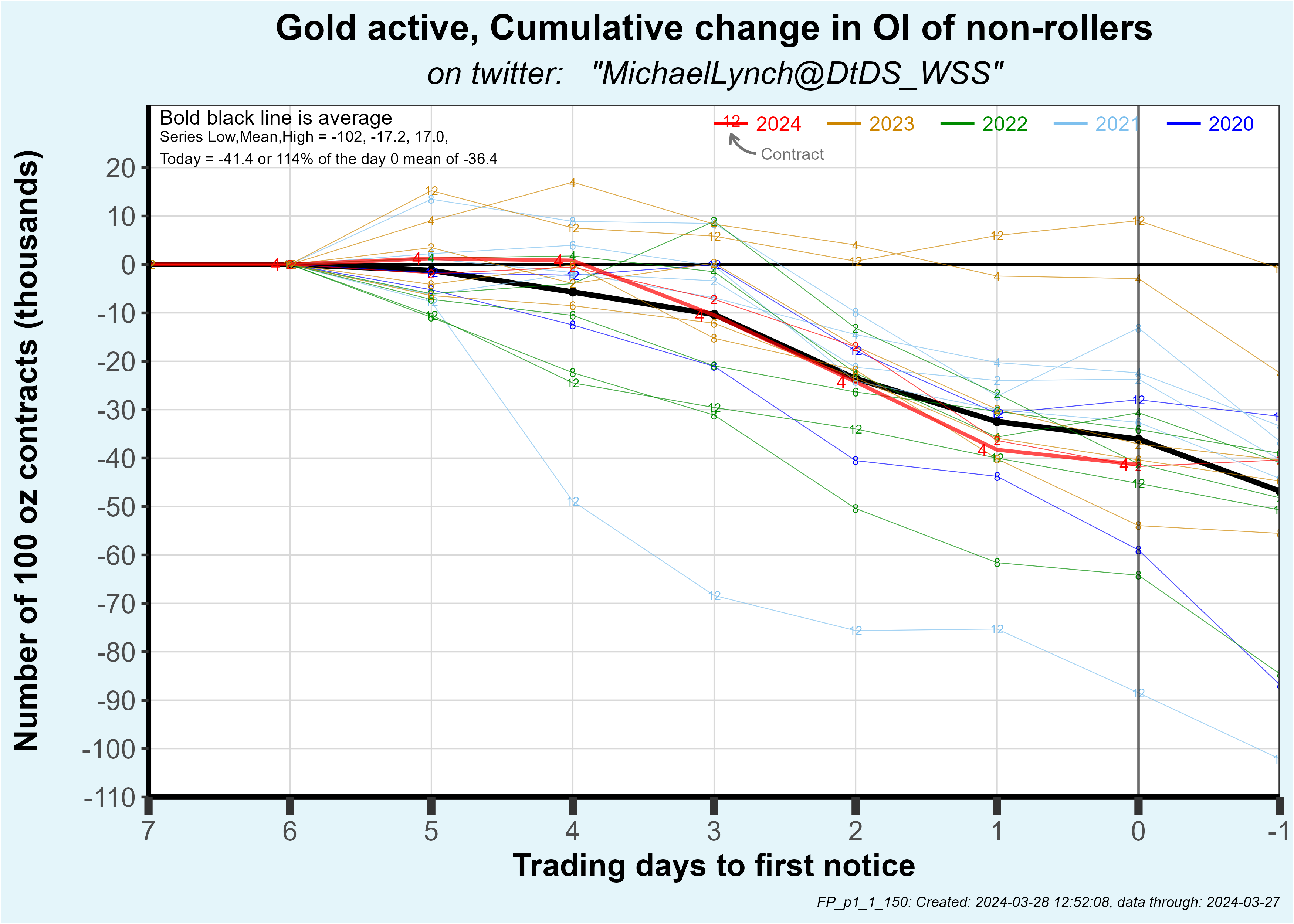

To understand this dynamic I track the difference between contracts closing on the roll month less contracts opening on the incumbent month. Over the last 6 days before first notice it typically totals 36,400 contracts on average (see below). That would be 3.6 million oz of gold or $8.0 billion of notional value at today’s gold quote. That’s some serious jack, so I believe it is mostly bullion banks.

The reason I bring this up is that I believe bankers drive the OI trajectory in the final days before first notice. In the case of this April contract, 41,400 contracts closed in the final days … 5,000 contracts more than the usual 36,400 contracts.

Note that this 41,400 “discretionary” contract closings in the final days before first notice dwarfs the 14,426 that actually stood for delivery.

I’m theorizing that bankers have the ability to assess market conditions in real time and adjust the number of contracts to stand for delivery.

So if more bankers closed in the final days than usual, wouldn’t we see a dearth of bankers on the issues and stops report?

There is, in fact, a dearth. Zero banks issuing delivery notices is a dearth.

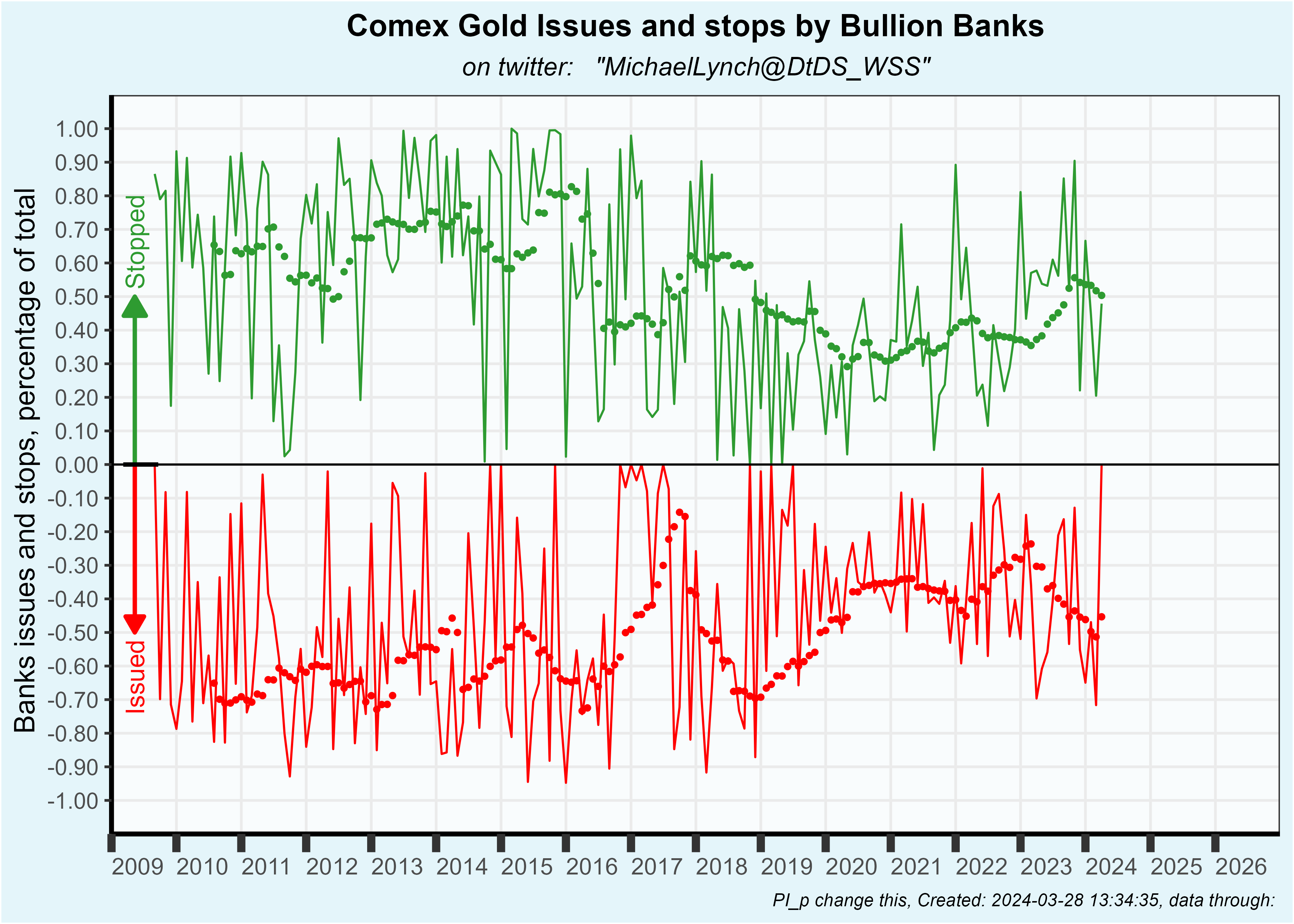

I just made the plot below this morning and it isn’t yet properly labeled, but deal with it soldier. It shows the gold bought or sold by bullion banks as a fraction of the total. The lines are the monthly data and the dots are a 12 month moving average.

Note that the bullion banks issued zero gold on the April contract.

This isn’t common. Since QE infinity (March 2020) only one contract was similarly low and that was June 2022 contract where bullion banks issued only 1% of the total. Interesting that June 2022 contract also came into first notice after a strong gold rally.

So … the bankers stood down on the April contract and closed their gold short positions, possibly in the final days before first notice. It’s possible that the banks closing shorts (by buying long contracts) contributed to the recent strength in the gold price. This theory explains a lot of data plus the recent gold price strength.

Let’s go with the theory … banks ceasing gold selling is a bullish signal. It’s even more significant given that this gold selling ceased in the aftermath of a $200 /oz rally. If that holds, how much longer can it be until panic buying is triggered?

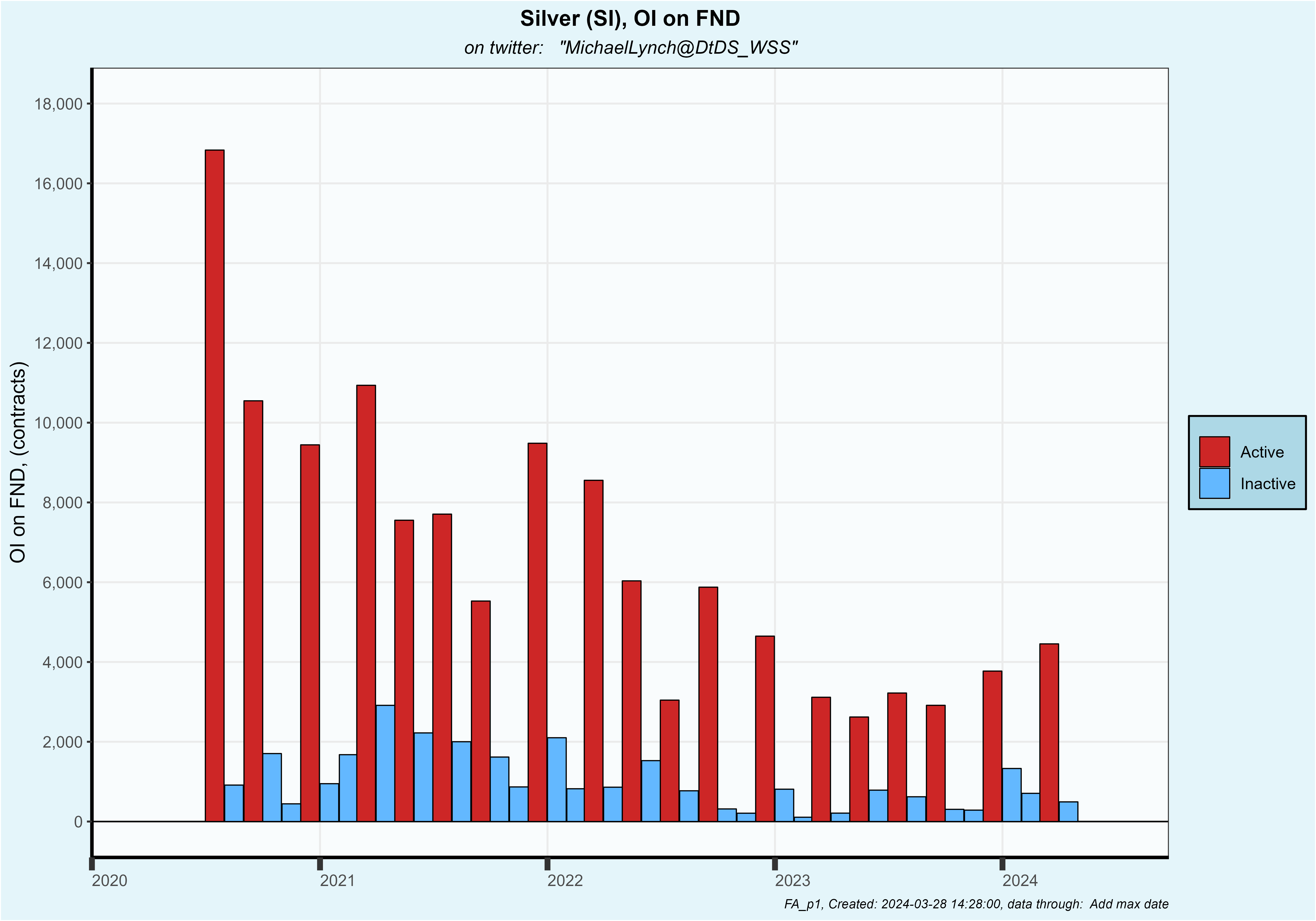

Moving on … even after the exit by bankers, the OI on first notice day remained on par with the prior 2 active month contracts:

The 14,426 contracts standing for delivery are 19% of registered which is the highest since June of last year:

As I said the bankers were absent from selling, but were present on the buy side of the transactions although it was no stampede:

Bank of Montreal stopped 1,471 contracts on the first day. BMO has accumulated a net 943 koz since QE infinity so this is a continuation of their significant accumulation.

Scotia stopped 799 contracts and Wells Fargo stopped 236 but both of those banks routinely flip metal, so there isn’t anything to discern from those amounts.

BofA stopped 2 contracts! While that is an inconsequential number, it tells me that BofA had zero shorts on first notice day. That is important as that is a change of direction for the biggest metals player at comex.

And … FYI, BNP Paribas is a bank, and they sold 150 koz of gold, but this is a rare gold transaction for them and I don’t consider BNP a bullion bank.

+++++++++++++++++ Silver

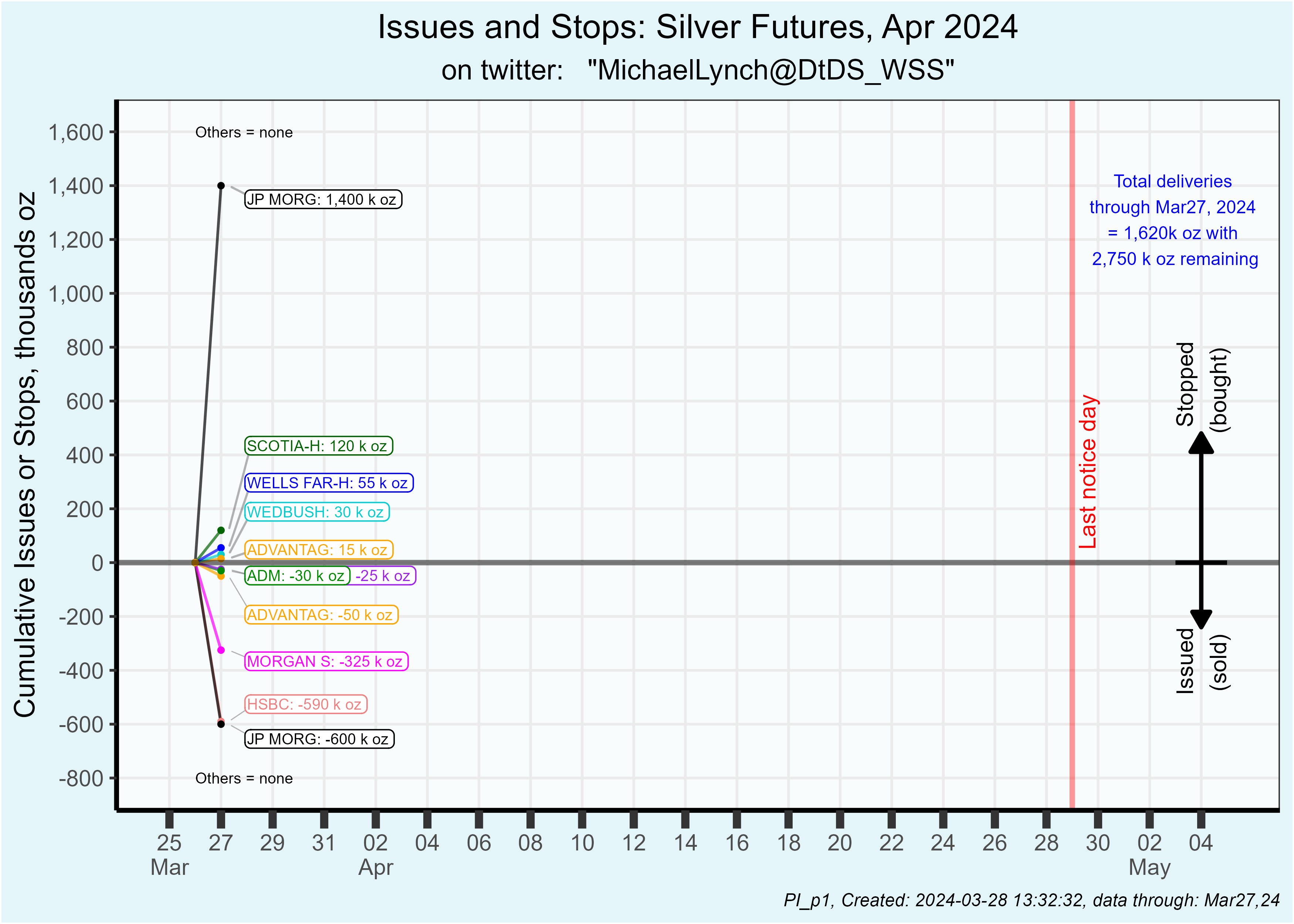

April silver had 493 contracts stand for delivery which was less than the prior two inactive contracts. Recall my post from yesterday which showed the largest one day OI reduction in at least 3-1/2 years. It appeared to me that longs were incentivized to close.

324 delivery notices were issued on the first day which is 66% of the total standing for delivery. That is high than usual so my naked short alert didn’t turn red.

That HSBC “customer” account issued 118 delivery notices or 590,000 oz. This is the 5th month in a row where HSBC is a dominant seller. The silver market would be very different if this customer hadn’t arrived.

JP Morgan customers issued 120 delivery notices. They also stopped 280 which was 86% of the total.

Silver continues to be a “market” of few players.

+++++++++++++++++++ Silver Vaults

Asahi’s vault had 580 koz transfer into registered which matches the 118 delivery notices issued by the HSBC “customer” account and also matches 580 koz moved into the vault the day before.

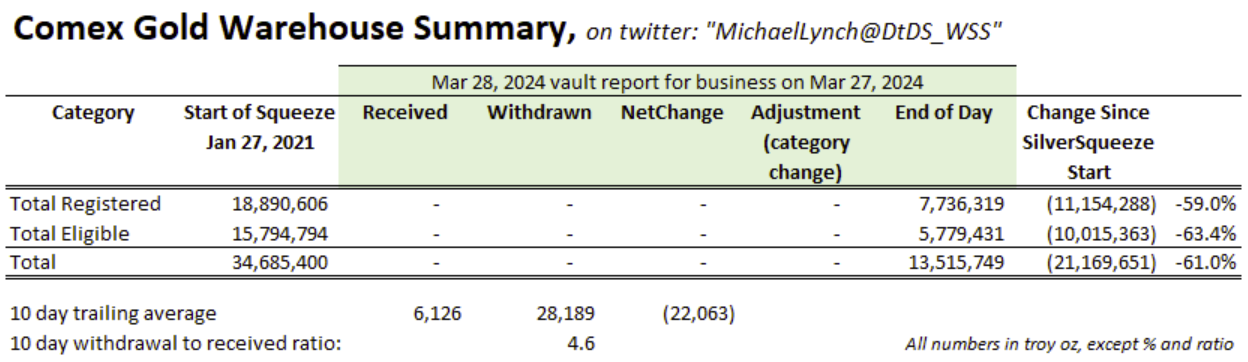

+++++++++++++++++++ Gold Vaults

No moves at the gold vault. This fits into my model that little gold is being moved into the gold vaults, deliveries are being made from metal already stored at comex and then is being removed at nearly the rate it is being bought. I covered that in this post:

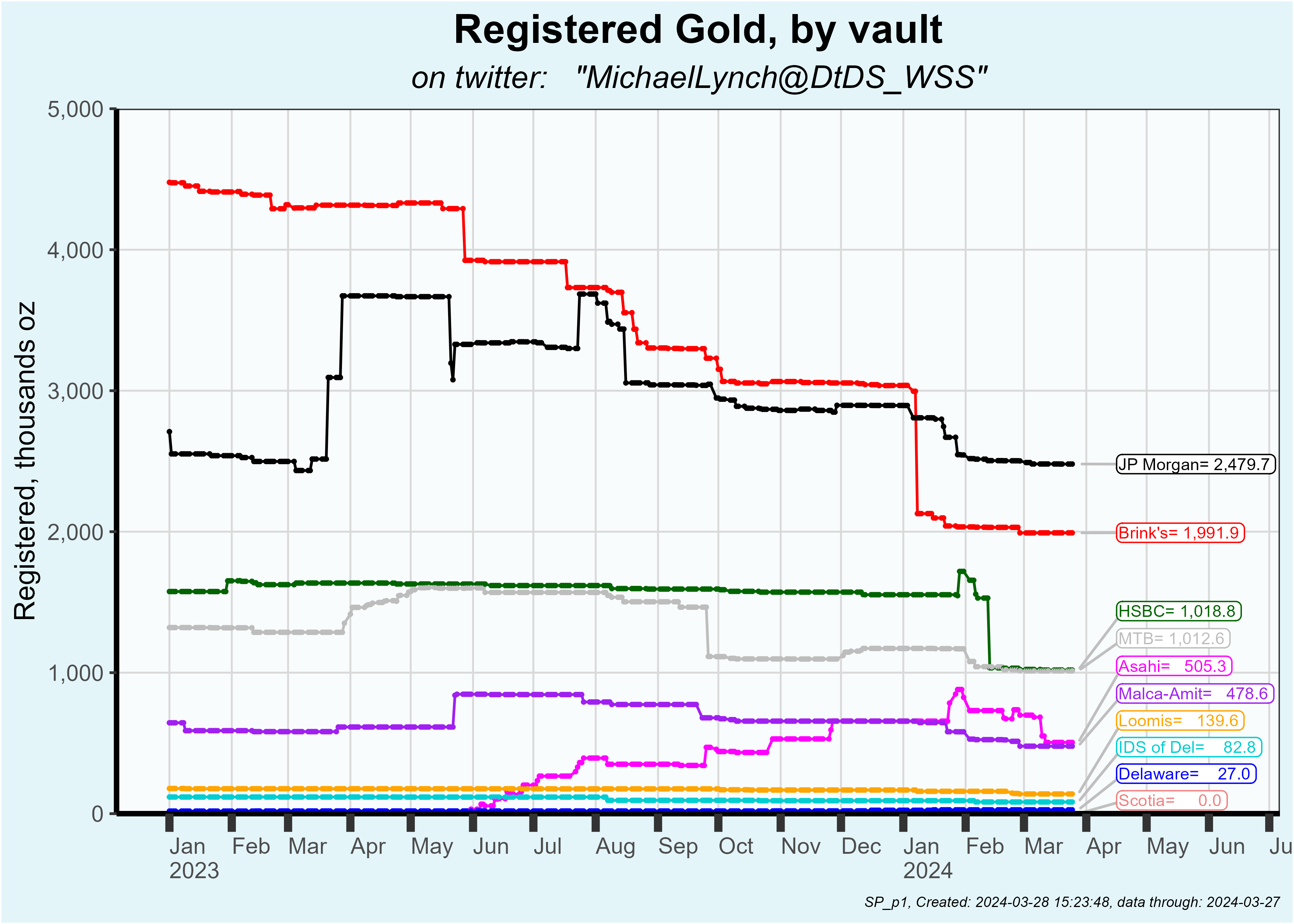

The numbers to the oz:

Nothing arriving at comex registered even though delivery notices were issued for 4.8 tonne:

Central banks are buying a lot of gold. Are they sourcing some of it through the COMEX?

Or are COMEX 100oz bars not what central banks are looking for, preferring 400oz London Good Delivery Bars?

Burn baby burnnnnnn!!