June silver contract has blowout off exchange shenanigans. A private account (Macquarie) fleecing HSBC? Is HSBC out of physical?

June silver contract has blowout off exchange shenanigans. A private account (Macquarie) fleecing HSBC? Is HSBC out of physical?

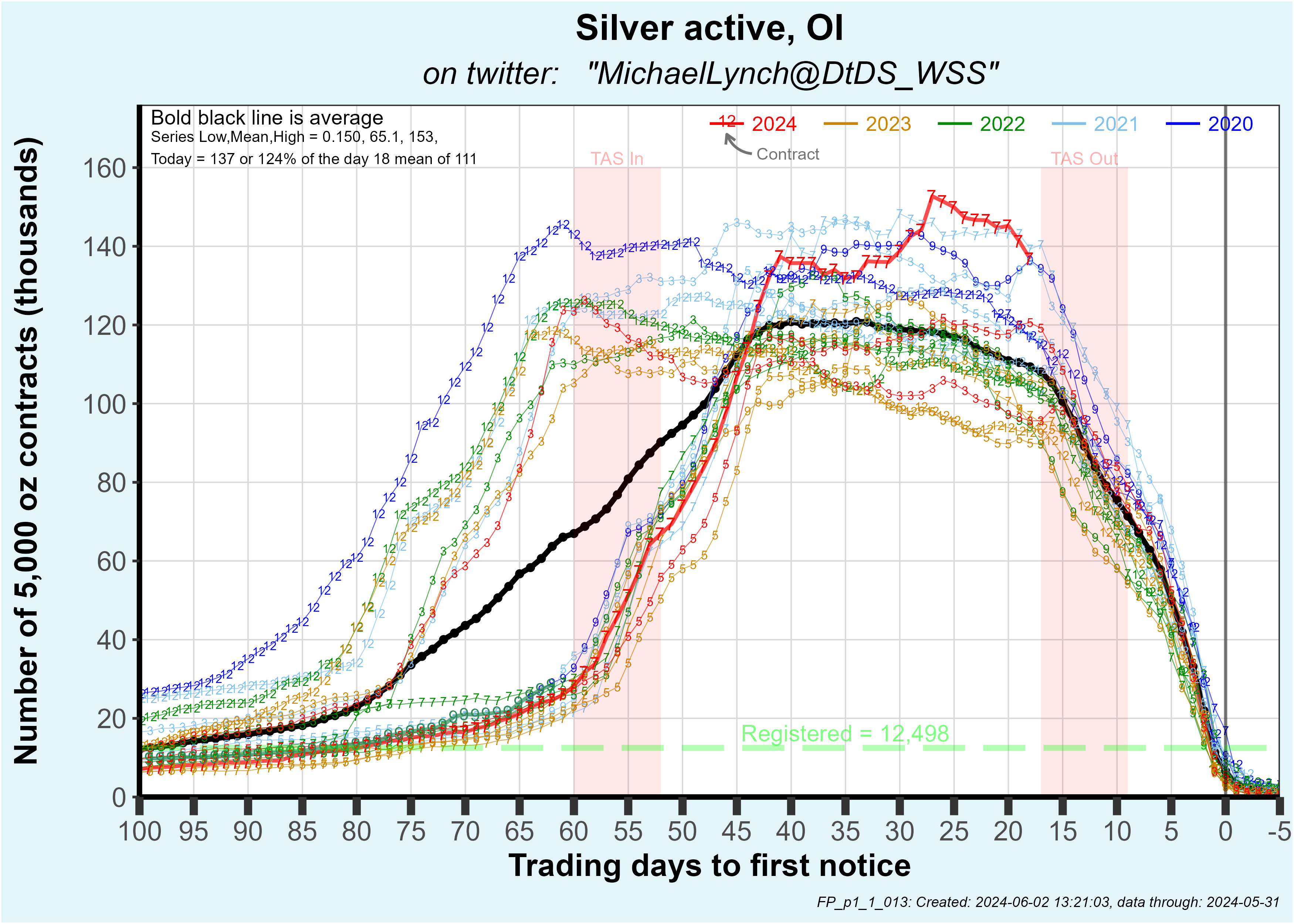

Plus, July silver open interest is menacingly high

I’m back in the saddle after some great hikes in the southwest USA. Taos NM is great for that as you can hike into the heat of the canyon of the Rio Grande one day and into snow capped peaks the next. But let’s get on with it …

+++++++++++++++++ Silver

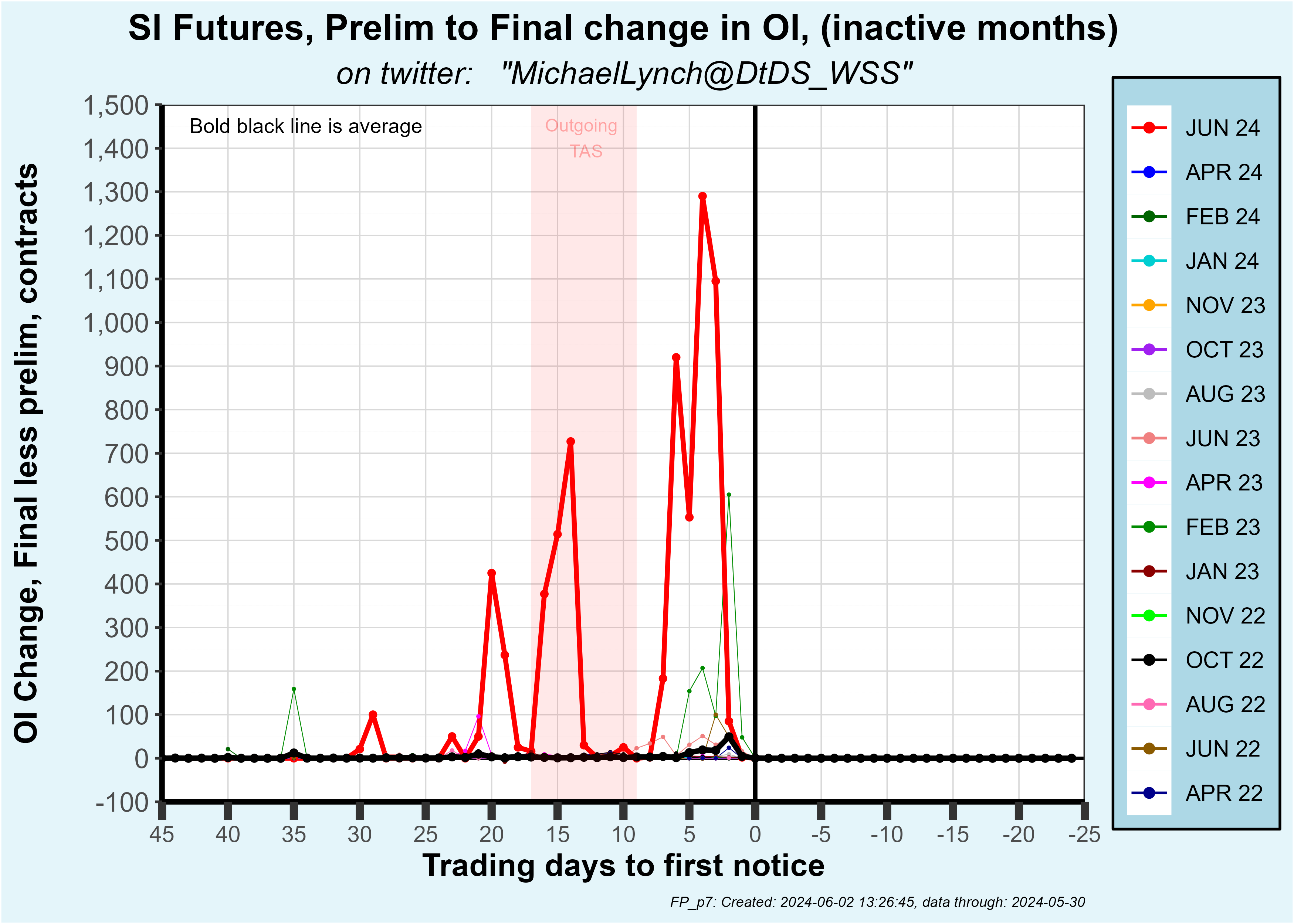

Earlier I had wrote about the extreme midnight shenanigans occurring on the June silver contract. It got even greater in the final days 7 trading days of the contract… far into record territory.

As a reminder, “midnight settlements” are my terminology where contracts settle off exchange between the preliminary print and final report. This change in open interest between those reports is typically very small likely representing minor accounting fixes. That changes in times of stress. In the case of the June contract a high fraction of the OI was vanishing indicating much more than minor accounting changes. These are contracts being settled off exchange.

The plot below shows the OI reduction between the prelim report and final report for each day. Note that most of the time the reduction is zero or nearly zero, so that data plots on the zero mark. Also note the obvious … the blowout reduction for the June contract:

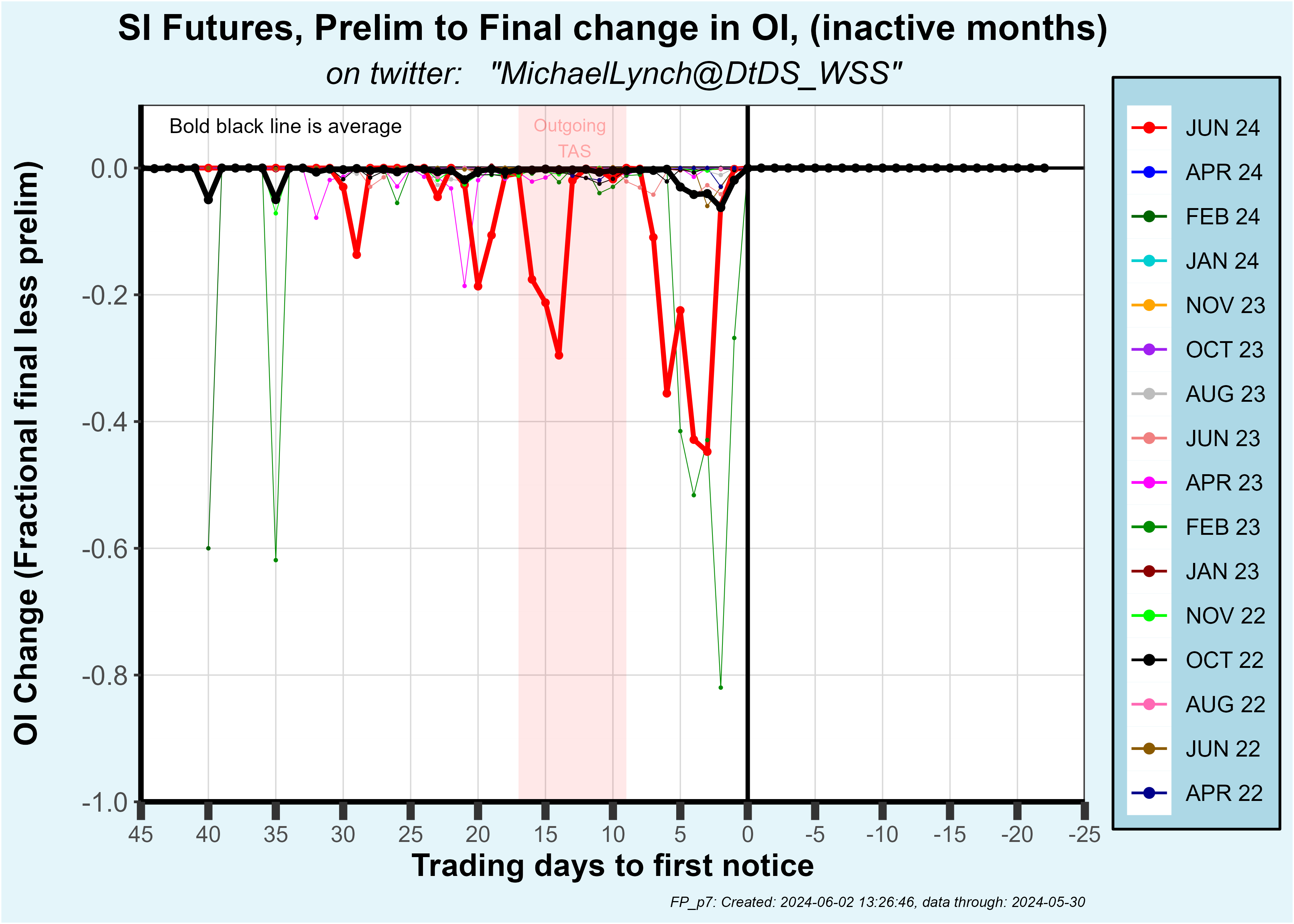

Looking at the same data as a fraction of open interest, you can see that for a 4 day period between 6 to 3 days to first notice, 22 to 42% of open interest vanished each day:

In total 6,732 contracts settled off exchange with midnight trades. That represents 33.7 million oz of silver.

I don’t believe that this number of contracts would have stood for delivery had the midnight settlements not occurred. What was likely occurring is that the short was initiating the midnight settlement and paying the long a premium to settle off exchange. After the long pocketed that extra fiat, he likely repeated the process. In this scenario the same long(s) would have counted for multiple trades inflating the number of midnight settlements.

Regardless … this is an indicator that there is stress at comex silver AND the displayed price is not the true market. Physical settlement is what justifies comex’s mostly paper trading market. If most of settlements are off the exchange at a different price to avoid physical settlement, then what meaning does comex’s posted price have?

Nothing.

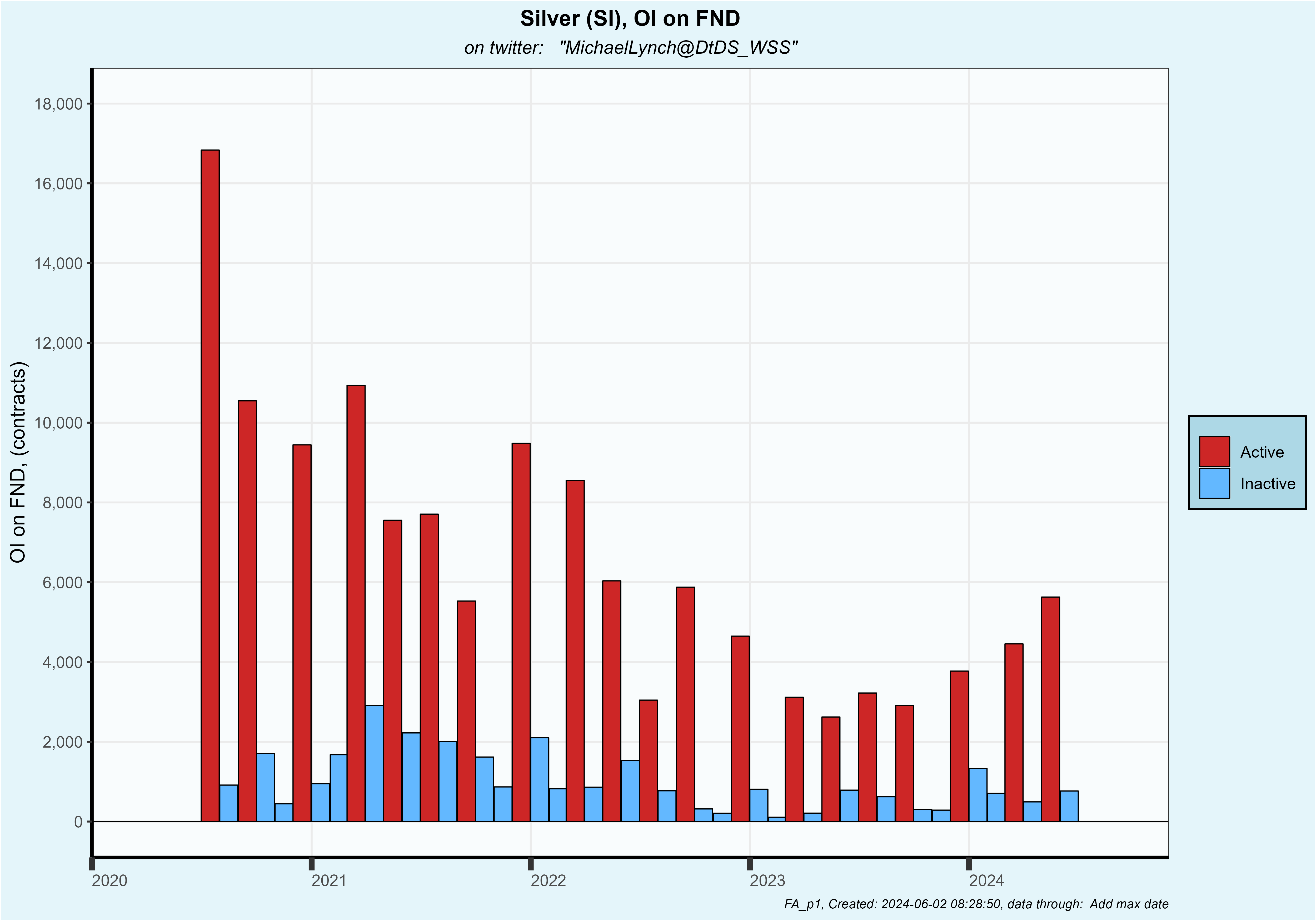

At the end of those settlement games, 766 contracts (3.8 million oz) stood for delivery (plotted below). Since the maximum June contract open interest was 2,013 contracts (10.1 million oz) it’s conceivable that this charade knocked 6.3 million oz off eventual deliveries.

Regardless, the 766 contracts is up 55% sequentially and the second highest in the last year.

It’s important to point out that if a long was determined to buy physical, all they would have to do is buy a contract, decline any coercion to settle off exchange and then stand for delivery.

However, the big unknown is … what level of coercion occurred? What price were the longs settling contracts at midnight? If it was a nickle over … not too big of a deal. If it was a buck or two … that’s a big deviation from the comex pricing charade.

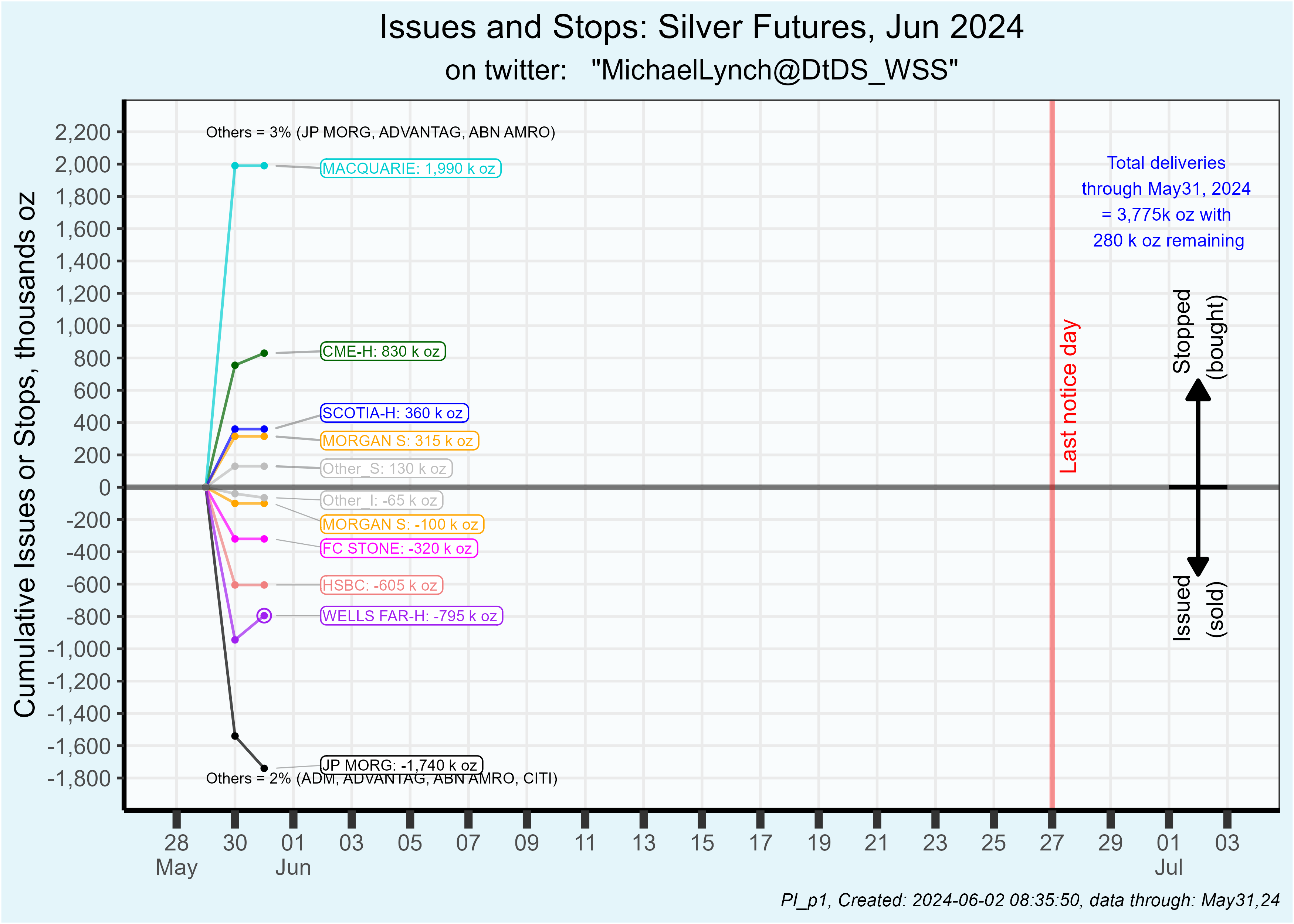

Moving on to issues and stops … Friday (May 31) was the second day of issuing delivery notices and delivery notices have been issued on 96% of the contracts that stood for delivery.

Typically it is apparent who were the big players on an inactive contract since most of the open interest doesn’t close and roll as occurs on active month contracts. Subsequently, as metal is delivered, the organization names get posted on the issues and stops report for both longs and shorts, so you know who was driving the market.

However in this case I may never know since such a high fraction of contracts were settled off exchange. If the short who was settling off exchange settled ALL his contracts, then there would be no contracts to settle and his settlement won’t be recorded on the issues and stops report. It’s conceivable that the market manipulator will remain unknown.

With that in mind, the list of shorts is less interesting than usual. JP Morgan’s customer accounts were the biggest seller at 1.74 million oz. The HSBC “customer” account, who has been the dominant short for 6 months, only sold 605 koz. I have to wonder … is that all the silver HSBC has? Maybe they’ve hit the bottom of their stack and resorted to settling for fiat?

If you’re new to my thread, I’ve advanced the idea that HSBC is manipulating prices down at comex while accumulating metal at other non-price setting venues. I called that the “differential lag theory”:

https://x.com/DtDS_WSS/status/1789023090065723627

To stack conjecture on top of conjecture … if HSBC has switched from dumping physical metal on comex to settling with paper at comex, this could be an indicator that their ability to contain comex price with physical sales is over. That would be a bullish signal, possibly very bullish.

Looking at the longs … the name that jumps out is the Macquarie customer account who bought 1.99 million oz. This is the second 2 million oz buy in a row … not typical for that account:

Since Macquarie was the largest long by far, I suspect they were the ones settling off exchange. Why? Only a party willing to take delivery would take the risk of buying a contract in the days before first notice. Otherwise, if the short (HSBC) didn’t offer to settle off exchange, they’d be stuck with the contract and on the hook for delivery.

My guess is that it was Macquirie fleecing HSBC. Plus they picked up another 2 million oz. If so, good for them … a private party beating a bank at their game.

Looking ahead to the July contract … OI stands at 136,629 which is only bested by July 2021 which was an infamous contract … the one which gelded JP Morgan.

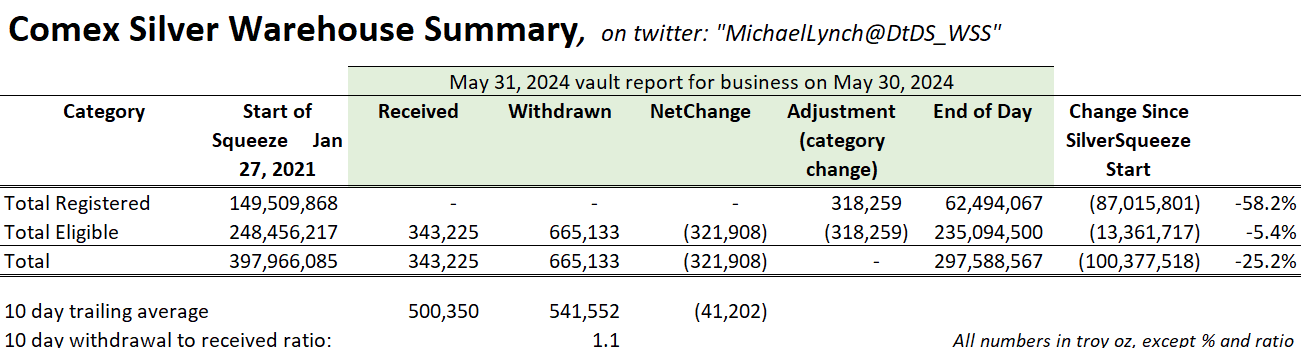

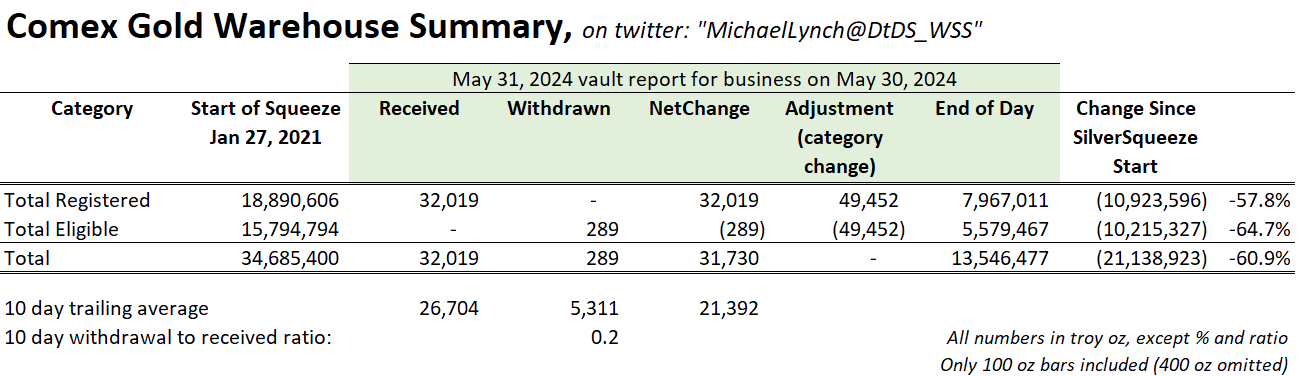

I’ll catch up on gold and vault activity tomorrow. The snapshot on the vaults:

+++++++++++++ Silver Vaults

+++++++++++++ Gold Vaults

Great to have you back - all rested and ready to report on pre-launch shenanigans and summer pyrotechnics.

Great to have you back. The banks that are short tried like hell to tamp silver down this morning and have failed so far. Are they running out of ammo?